Shan N: The Keynesian Playbook – Eat your Cake and Have it too!! Are we at the End of the Road?

/script type=”text/javascript” src=”https://app.getresponse.com/view_webform_v2.js?u=S6bT5&webforms_id=A25R”>

Guest post from Shan N., an Economist based in India. He is the author of the recently published book “RIP U$D: 1971-202X …and the Way Forward” and can be contacted at shan@plus43capital.com

—

Prologue: The adoption of Keynesian Economics by policymakers worldwide is now so absolute that the observation of Milton Friedman that “We are all Keynesians now” is almost a truism.

Yet, if the Austrian School/Lassiez Faire Economists are to be believed, the US and many parts of the world are teetering on the edge of inflationary depression. The final outcome of this economic crisis could well be one in which most currencies go down the route of the German Papiermark.

Which begs the question: If Keynesian Economics is so fundamentally flawed, what explains the rather widespread growth of the last few decades? Financial Assets (stocks and bonds) have done spectacularly well, and notwithstanding the 2008 GFC, real estate has also done well. As far as Price inflation is concerned, it has been relatively benign for most periods in most parts of the developed world. What explains this prosperity?

It is certainly a good question, and this article addresses it. I think the crisis itself is inevitable, and not much can be done about it at this late stage. But I do hope we don’t embark upon making the mistakes of previous decades on a more grandiose scale as we did after the 2008 GFC.

Introduction: For the last 35 years, the US, in particular, and the world in general, have relied on the Keynesian playbook at every hint of trouble—the 1990s Gulf crisis, the Nasdaq bubble burst, the 2008 GFC, and COVID–19. In all these crises, the go-to solution has been loose monetary policy.

For the first few events, the solution was a reduction in the Fed funds rate, and when that was not sufficient, the rate cuts were accompanied by an expansion of the Fed Balance sheet, aka QE (Quantitative Easing). Even Keynes wouldn’t have imagined this extensive use of his rationale—if you can call the Keynesian recommendations a rationale in the first place.

The Keynesian Playbook – Though there are multiple versions practiced today, John Maynard Keynes advocated using monetary policy to manage/stimulate aggregate demand and thus smoothen the business cycle. In his book “The General Theory of Employment, Interest, and Money”, he advocated running deficits during times of recession and surpluses during good years to pay down the debt. Given the compulsions of democratic politics, deficit financing has become a permanent feature of almost all governments today.

Keynes wrote his book in 1936, supposedly as a solution to end the then-ongoing Great Depression. Of course, most of his assumptions regarding what caused the Great Depression were utterly wrong. Murray Rothbard’s “America’s Great Depression” accurately describes the causes as the highly interventionist policies (by the then-prevailing standards) of Herbert Hoover and Franklin Roosevelt as a response to the stock market crash of 1929.

Andrew Mellon’s advice (the then Treasury Secretary) – “Liquidate labor, liquidate stocks, liquidate farmers, liquidate real estate. It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up the wrecks from less competent people.” – is often quoted to indicate the Lassiez Faire approach taken by Hoover. But as Rothbard explains, Hoover completely ignored the sage advice of his treasury secretary.

To add insult to injury, Roosevelt, confiscated Gold from US citizens in 1933 through Executive Order 6102. These and other acts were a far cry from the “Capitalism / Free Markets” policies that Keynes believed the US Government was operating under.

As Rothbard explains in his book, these fiscal and monetary interventions prolonged what ought to have been a short recession into The Great Depression. Jim Grant’s book “The Forgotten Depression:1921: The Crash that Cured Itself” would be most appropriate to understand the correct policies to treat an economic downturn. The Government under Warren Harding in 1921 allowed the market corrections to run its course, and the malinvestments were cleared quickly. Incidentally, these excesses were created due to the monetary interventions of World War I (1914-1919), during which the National Debt grew at an unprecedented CAGR of 55+%. The monetary excesses that caused the 1929 crash were substantially lower in comparison.

Despite the above-mentioned monetary interventions, these remained exceptions to be implemented only under what was seen as extenuating circumstances e.g. World War and The Great Depression. Keynes’ policies based on “deficit financing by Central Banks” could not be implemented under the Gold Standard during normal situations. Even the diluted version, i.e. The Gold Exchange Standard of Bretton Woods, limited the interest rate manipulations and the borrowings by the Federal Government.

Hence, it’s unsurprising that Keynes referred to Gold as a “Barbaric Relic” as it prevented widespread adoption of his policies. But what is surprising is that while most Economists and Central Bankers have adopted the Keynesian playbook as a policy tool, they continue to retain Gold in their reserves—albeit nowhere close to a level where they can back their issued currency with the gold they hold.

It would not be until the 1960’s that a modified version of the Keynesian Playbook would be attempted in the US. It was the period in which the thought process of “a little deficit spending is good” developed amongst economists. The effects of such principles were very visible in the National Debt growing at a cumulative 30% during 1960 to 1970 as compared to just 11% in the previous decade of 1950 to 1960. It is this deficit spending during the 1960s that prompted the “hard money nations” to trade their US Dollars for Gold and one that would eventually make Richard Nixon “temporarily” close the Gold Window in 1971. Incidentally, when the Gold Window was closed (or, more accurately, when the US Government tried to demonetize Gold), Keynesian economists widely suggested that Gold prices would go to “Zero.”

The US would pay for this decade of deficit spending (1960s) with the stagflation of the 1970s. The 1970s stagflation should have made the Economists recognize that the Keynesian playbook was a very flawed one, i.e., indulging in deficit spending has severe consequences, though perhaps much delayed in terms of timelines. This monetary inflation masquerades as growth in the interim period, enabling profligate spenders to look smart. A good example would be Trump, who grew the National Debt by more than $7 trillion in his first term and took credit for the supposedly low price inflation.

| That there are no free lunches and all monetary inflation (i.e. deficit spending) would eventually show up as price inflation is just an economic axiom. The sooner the world recognizes that this deficit spending, or more appropriately, the growth in National Debt, is “The Inflation,” the better it will be. The Monetary Inflation that the world initially loves, is exactly the one that produces the Price Inflation that the world hates. |

Incidentally, many still believe that the US operates as a Capitalistic system though it ceased being one more than 100 years ago with the formation of the Federal Reserve in 1913. Whatever remained of “the unalienable rights of life, liberty and the pursuit of happiness” that made the US the industrial powerhouse was laid to rest in 1971. What is left today is an empire in financial and moral ruin that threatens and enforces its will by removing inconvenient Governments / political leaders by overt and covert means. From being the engine of growth and liberty in the 19th century and a substantive part of the 20th century, the US today is the engine of monetary inflation and military confrontations worldwide.

Returning back to Keynes, if the limited monetary inflation of the 1960’s, caused the stagflation of the 1970’s, when what would 3 decades of massive monetary inflation from the 1990’s lead to? But before answering that, it would be necessary to understand the rather prolonged cycle of benign price inflation we have had from 1990 till 2022.

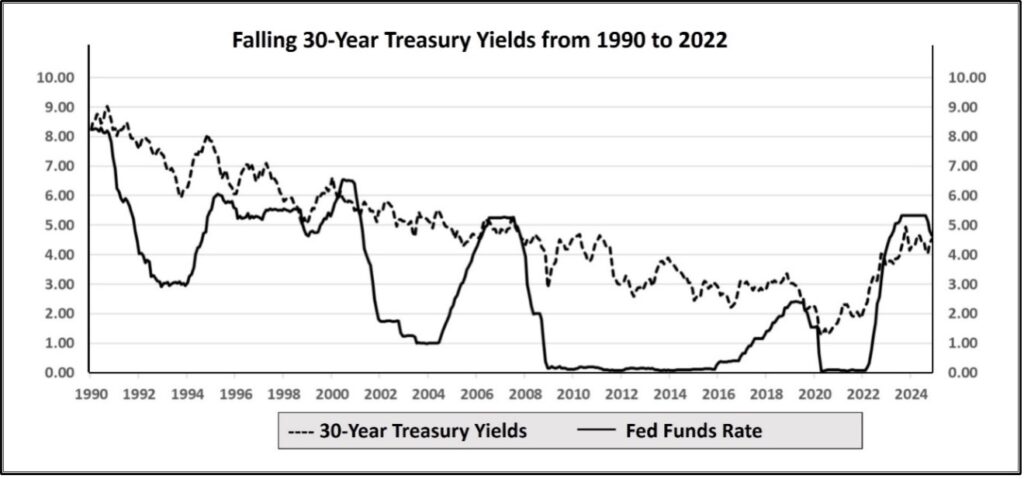

Here are some interesting observations from the graph above that show the trend of 30-year Treasury Yields and the Fed Funds Rate from 1990 to date.

- The 30-year rate peaked in Aug 1990 at 9%. It bottomed in July 2020 at 1.2%.

- For 30+ years, the markets have been subjected to muscle memory of falling 30-year Treasury yields.

- The upswings in rate we have had in the above period were limited and for a short duration.

- Between 1993 and 1994, the rate went up by 2.0% over a 12-month period.

- Between 1998 and 2000, the rate went up by 1.5% over a 27-month period.

- Between 2008 and 2010, the rate went up by 2.0% over a 15-month period

- The more than 3.8% increase over the current 54 period starting July 2020 is the maximum strengthening of the 30-year yield the markets have witnessed in the above period. While bond veterans would know that this is not a substantive increase by any measure, for investors conditioned to falling yields, this is indeed a very unexpected event.

But was this prolonged period of 30-year rates falling a natural market event? Not by any stretch. To a large extent, the Fed Funds rate determines the 30-year rates, which is a direct correlation. But beyond these, the US Fed indulged extensively in Operation Twist to flatten the yield curve post-2011. The price inflation numbers have also been grossly under-reported in the US to create an illusion of price stability thereby aiding a lower rate environment.

This prolonged 15+ years of low interest rates since the 2008 GFC —ZIRP at the short-end and sub 5% at the long-end, allowed for the build-up of the enormous National Debt. During the decade of 2010 to 2020, the National Debt doubled compared to the 30% growth during the 1960s. The debt “appears” serviceable only because of the low rate of the National Debt at 3.3%. But even at this low rate, interest payments as a % of the Federal Revenue is well over 25%. What will happen when this interest rate goes to 5% in a year or two, and that too at a period when the National Debt is ballooning by the day?

The Death Knell for Keynesian Economics

In almost all situations in life, effort comes before reward. Through deficit spending in the name of public welfare, Keynesian economics provided an academic cover for a scheme where the fruits could be enjoyed today, and the price would be paid by citizens tomorrow. The US Government, as the owner of the reserve currency, had the power to abuse this privilege the most. That said, almost all nations have been party to this scheme to varying degrees, almost without exception.

One of the greatest ironies of welfare schemes is that they are almost always financed through the Inflation tax (i.e. deficit financing). When a Government gives a certain amount conspicuously to the poor, it usually takes away surreptitiously from the very same recipients through the reduced purchasing power of their currency.

Central Bankers, through their monetary tools (QE, TWIST, etc.), ensured that the party could continue for decades. But as in life, there are no free lunches, and there will come a period when the effects of monetary inflation show up in price inflation. The central bankers can postpone/delay the inevitable, but the payment has to be made at some point. The longer it is delayed, the bigger the bill becomes.

What lies ahead for the US Economy and most parts of the world is not pretty. It is going to be a heightened version of the stagflationary 1970s – deeper recessions and greater price inflation. The Volcker solution of jacking up the interest rates is almost impossible as the National Debt is not even serviceable today at the prevailing 3.3% interest rates.

But at least theoretically, the solution is remarkably simple – a massive reduction in government expenditures to balance the budget and a return to the US Government’s foundational principles of limited government and sound money (i.e. the gold standard). This applies to all governments without exception, and whether the US takes the lead or not, other countries, in their enlightened self-interest, should adopt this route. Balancing the budget can be done today. Javier Milei, the current Argentinian President and a democratically elected one at that, did this in 6 months flat. Maybe other countries can take double the time. The Gold standard can and will follow automatically tomorrow.

Epilogue – Keynes was knighted in 1942 for his “contribution” to Economics. But the damage to the world in the decade(s) ahead due to the widespread adoption of the Keynesian playbook is going to be worse than the combined damage done by Stalin, Hitler, and Pol Pot. The day Keynes is de-knighted might well indicate the light at the end of the long, torturous, and a very dark tunnel ahead.