Interest payments on just federal government debt now exceed the entire Defense Department budget

Unsustainable. The country is going bankrupt. Trump is the only path forward.

CBO: Federal Interest Payments Now Exceed Defense Spending (Forbes)

Federal Debt: The Ticking Bomb in Your Wallet

By: Heritage, July 19, 2024

Grab your pay stub for June and see how much you paid in federal income tax…over 75% of that was effectively your contribution to interest on the debt last month.

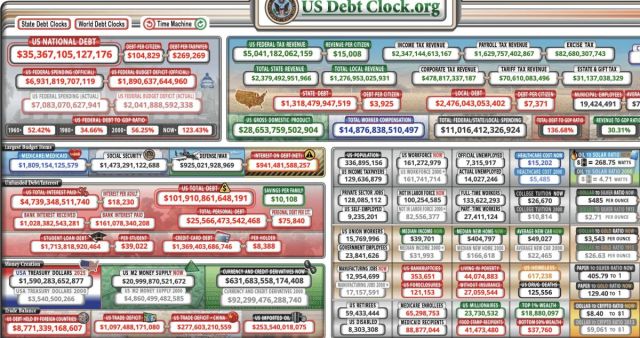

This is where our federal government is today. It has spent so much more than it has taken in that it has racked up a $35 trillion debt.

The time bomb of federal finance has already started ticking down.

Copied

If you don’t think the interest on the federal debt is a problem, try this quick exercise. Grab your pay stub for June and see how much you paid in federal income tax, then realize that over 75% of that was effectively your contribution to interest on the debt last month. No roads, schools, military or hospitals—just interest. Houston, we have a problem.

For the first time ever, the government spent $140 billion in a single month to service its gargantuan debt of nearly $35 trillion. By the end of this fiscal year, the Treasury will spend almost $1.2 trillion in interest alone. And the problem is getting worse.

For June, not a single line item in the Treasury’s monthly statement was larger than the $140 billion interest expense. It was larger than either the Social Security Administration ($129 billion), Department of Health and Human Services ($90 billion), Department of Education ($87 billion) or Department of Defense ($63 billion).

>>> Trump’s Record Far Superior to Biden’s on Debt and Inflation

Interest is now equal to more than three-quarters of all personal income taxes, and over 30% of all taxes and duties received by the Treasury in June. Not only is the nation drowning in debt, but now the interest payments are an anchor around its neck.

Federal finance can seem a bit ephemeral, so let’s put this in terms of family finances. Imagine a family has racked up more credit-card debt than it earns in an entire year. Those cards had low introductory interest rates, so even as their debt ballooned, the monthly interest payments seemed manageable. But then, rates rose—and so did the finance charges.

Because the family spends more than they earn each month (hence the massive credit card debt), any additional expenses only exacerbate their financial nightmare. Higher interest is just another expense that must be financed, which means their outstanding balances will now grow that much faster.

Of course, higher balances mean higher finance charges, and the debt doom loop has begun. The family has no way out other than severe spending cuts in their budget or an ignominious bankruptcy.

This is where our federal government is today. It has spent so much more than it has taken in that it has racked up a $35 trillion debt. It’s not only many times larger than annual federal tax revenue, but over 20% larger than the nation’s entire economy.

One key difference, however, between the family budget and the federal budget is counterfeiting. For the family, this isn’t an option—unless they want to go to jail. For the federal government, creating money is the preferred way to conduct a backdoor default on its obligations.

Article posted with permission from Pamela Geller